What Is the Real Difference Between Roth IRA and 401(k) in 2026? (Smart Guide to Choosing the Best Retirement Account for Tax Savings and Long-Term Wealth in the USA)

Business & Finance

Learn the difference between Roth IRA and 401(k), and how to choose the best option to reduce taxes and grow your retirement savings in the USA.

Roth IRA vs 401(k): Complete 2026 Guide

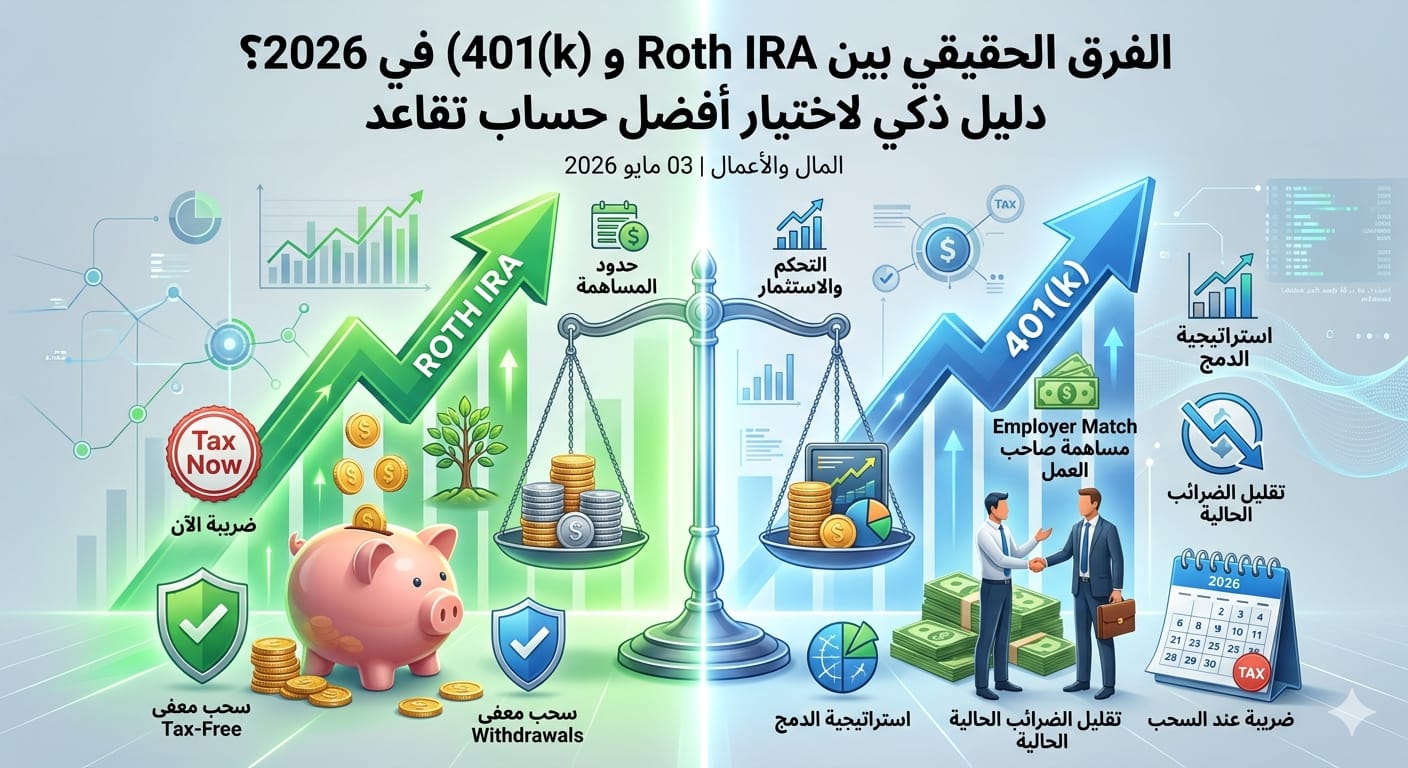

The key difference between Roth IRA and 401(k) is tax timing. A Roth IRA uses after-tax contributions with tax-free withdrawals in retirement, while a 401(k) typically uses pre-tax contributions with taxes deferred until withdrawal.

Introduction

If you work in the United States and are thinking about retirement, there’s one question that can define your entire financial future: Should you choose a Roth IRA or a 401(k)?

The decision is not simple, because each account has a direct impact on your taxes, investments, and retirement income.

The problem is that most content explains the difference in a theoretical way — without telling you when to actually use each one.

In this guide, you’ll get a practical breakdown to help you make a smart decision based on your income and long-term goals.

PART 1 — Core Understanding + Key Differences

What Is a Roth IRA?

A Roth IRA is an individual retirement account funded with after-tax money.

How It Works

You pay taxes now

You invest the money

You withdraw later tax-free

Ideal for long-term growth

What Is a 401(k)?

A 401(k) is a retirement plan provided by your employer.

How It Works

You contribute pre-tax income

It reduces your taxable income

You pay taxes upon withdrawal

Often includes employer matching

The Core Difference Between Roth IRA and 401(k)

The main difference is when you pay taxes.

Quick Comparison

Roth IRA → Pay taxes now

401(k) → Pay taxes later

Roth IRA → More flexibility

401(k) → Higher contribution limits

Which Is Better for Taxes?

It depends on your future financial situation.

The Golden Rule

If you expect higher income later → Roth IRA

If you want to reduce taxes now → 401(k)

Contribution Limits

A critical factor in your decision.

Key Differences

Roth IRA → Lower limits

401(k) → Higher limits

You can use both

Depends on your income level

PART 2 — Strategy + Smart Decision-Making

When Should You Choose a Roth IRA?

Best Situations

Lower current income

Early in your career

Expect higher future income

Want tax-free withdrawals

When Should You Choose a 401(k)?

Best Situations

Higher income

Want immediate tax reduction

Employer offers matching

Ability to contribute more

Can You Use Both?

Yes — and this is often the best strategy.

How to Combine Them

Start with 401(k) to get employer match

Then invest in Roth IRA for tax-free growth

Use both for diversification

Balance your tax strategy

Pro Strategy — Tax Diversification

A key strategy used by experienced investors.

Concept

Diversify account types

Reduce future tax risk

Increase withdrawal flexibility

Gain better financial control

Common Mistakes

Choosing only one account

Ignoring employer match

Not investing consistently

Thinking short-term

❓ FAQ (People Also Ask)

Is Roth IRA better?

Not always — it depends on your income.

Is 401(k) better?

Better for reducing taxes now.

Can I use both?

Yes — and it’s often optimal.

Which gives higher returns?

Investment choices matter more than account type.

Conclusion

Choosing between a Roth IRA and a 401(k) is not a small decision — it can shape your entire financial future.

The smartest approach is not choosing one, but building a system that uses both effectively.

Start today — because the best time to plan for retirement is now.